Price Transparency Predictions

Back in 2019, Oliver Wyman predicted that 2021 would be “the year of the consumer”. Price transparency -- and its accompanying sticker shock -- is merely the first step in helping consumers make smarter and more educated choices about their medical care, we said back then.

Well, here we are in 2021, coming out of the pandemic, and hospitals are now required to publish negotiated rates on how much their services cost. Large data releases have already begun. Organizations like Turquoise Health are emerging with consumer front-ends to curate the data. In many markets, consumers can now hop online to quickly comparison shop for medical services and look up the price of a coronary bypass, for instance, to see how much it would cost based on their insurance, coinsurance, deductible, and copay. Healthcare is finally taking steps to become more like the retail industry where the price of something is readily available at your fingertips (literally).

More accessibility means more data to analyze. Data released thus far reinforce what we’ve known all along—pricing variation levels are unjustifiably high. (At a single hospital in one part of the US, for example, a knee replacement can cost between $23,000 and $100,000. At others, some patients will pay 10 times what others pay.)

Specification around price transparency data releases remains incredibly broad; there’s much room for interpretation. This is naturally leading to a huge range of formats and pricing estimation approaches in the released machine-readable files. Another issue is compliance, or to be more specific, lack of it. A minority of providers are posting payer-specific negotiated rates.

There will likely be multiple rounds of rule adjustments before the industry sees broad comparability on any set of services. Frankly, contracting processes are so unwieldy among payers and providers that we should not expect universal transparency in any reasonable timeframe.

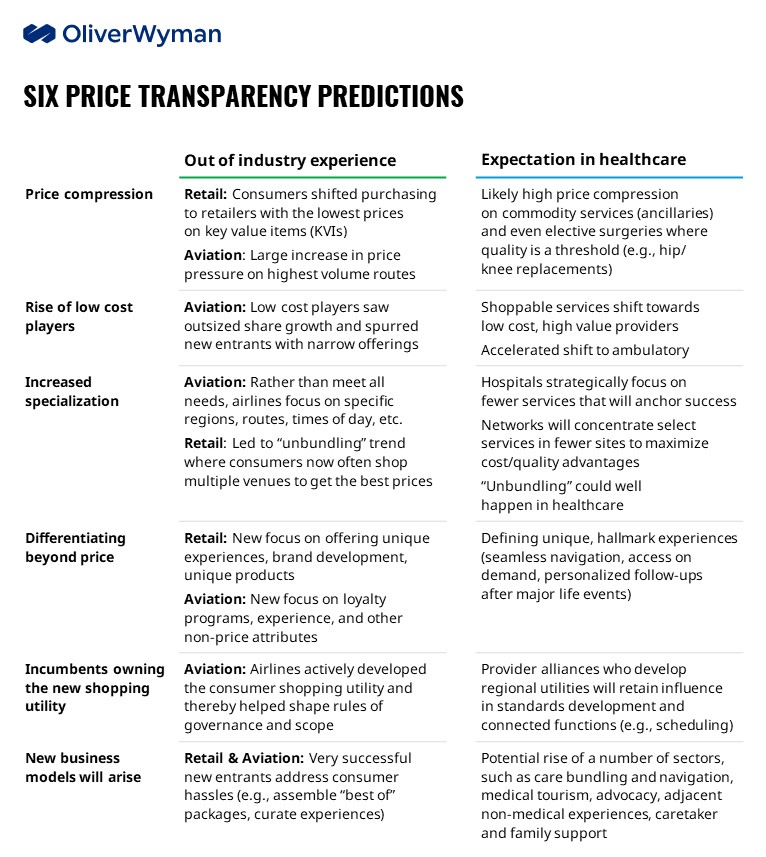

Six Price Transparency Predictions

If we take a step back and look at other industries that have faced abrupt introductions of price transparency, we can make a few predictions for healthcare. We believe that healthcare will face six key trends as prices become increasingly visible and comparable:

1. Price variation will compress on more shoppable items and may increase on less shoppable items

Once, there was a time without the widespread online availability of goods and services. Take online grocery shopping—now commonplace, especially given the pandemic. Before online grocery shopping, as a consumer, people generally made a physical list of what kind of food items they wanted to purchase when they physically went to the store. Consumers kept in mind the price of the most common item, including staples such as milk, bread, and butter (known as KVIs - Key Value Items). Harder to keep track of were less frequently purchased, or less commodity-like items like granola bars, sea salt, and the like. Retailers exploited this and engineered margin out of those products that are harder to track.

Then, e-commerce changed the dynamic. Now, you can scroll through every last grocery purchase you made and easily track and compare prices across retailers. It suddenly became fairly easy to rapidly compare the prices of everything in your online shopping across multiple local retailers. If the same item was 30 percent cheaper, for instance at another online retailer, this information could be found quickly and easily.

How This Would Look in Healthcare

Just as in retail, we expect that easily comparable services (i.e. those that are more “shoppable”) will see price compression. Commodity services such as ancillaries and even services where quality is a threshold, such as knee replacements or common GI procedures, will see consumers shift to lower-cost sites and providers, thus forcing higher-cost providers to close the gap. In parallel, those services that are less shoppable may see prices increase as providers look to maintain their profitability across their portfolios.

2. New platforms will amplify the voice of low-cost players

As new tools and platforms enter the market to make use of this data, consumers will increasingly use price as a factor in selecting where to receive services. This will amplify the reach of new and incumbent low-cost players, by helping consumers to face the dollar value they are attaching to brand-name, associated quality, and consumer experience of the alternate options. (We will address in a future article how we expect price transparency to evolve to value transparency.)

In aviation, you can tie the rise of ultra-low-cost carriers (ULCCs) like RyanAir and Spirit partially to the platform offered by online-booking sites, which challenged consumers to switch from the mainline carriers (even if only once) in the face of overwhelming cost savings. Enough of the switchers stayed, and enough new consumers tried each year, to make the ULCCs one of the strongest growth segments of the aviation industry.

How This Would Look in Healthcare

Within healthcare, we expect a similar trend as providers start competing on price for shoppable services that they can perform at scale to drive both cost-savings and improved quality of care. This will intensify competition in acute and ambulatory alike, as existing and new players seek to win by pulling services out of high-cost sites. Their consumer outreach will only be further amplified by a wave of platforms devoted to aiding consumers in navigating the newfound price transparency (see predictions #2 and #6). Where low-cost providers achieve defensible quality, they will represent a real threat to large-scale providers that aim to cover all services “in-house”.

3. Expect specialization in scopes of services

The aviation sector offers another interesting lesson for healthcare in the realm of specialization. At the end of the day, there are only so many ways to make a flight between Boise, Idaho, and Boston, Massachusetts a different experience, and so the question then becomes: which airlines exactly, are going to offer that service? The network designs of each of the carriers are one of the key levers airlines have for defining what “products” they put out into the market. Just as a health system may choose not to offer a full scope of Oncology services, an airline may choose not to offer a specific route, or may deliberately time a flight to be at a different time of day than a competitor—and thus less comparable.

In aviation, the result is that for a specific Origin - Destination combination, there are a finite set of carriers to choose from, and even fewer options as you start refining on key “product characteristics” like some connections and time of arrival/departure. The increased intensity of competition has led to specialization and a reduction in competitors on any given combination. Players who remain are those who can sustainably compete with that offering.

In retail, the rise of the “discount era” led to “unbundling,” where consumers began going to different players (like fresh-offering specialists) for the different goods and services they’d need.

How This Would Look in Healthcare

In healthcare, it will be increasingly hard to compete on broad scopes of services. The increased price transparency will almost definitely feed directly into decision-making on the suite of services a particular health system offers. Previous portfolio decisions that were made solely on internal information and general awareness of competitor’s services, will now be augmented by a directional understanding of how much competitors can charge for their “similar” services.

Health systems will focus investment on scopes of service where they can sustainably differentiate. For some, it will be women’s health. For others, heart care, and so on. Within a given system, it will lead to consolidation of services into fewer sites (for example, most all-elective orthopedic surgery will be in one facility) to maximize scale benefits for quality and cost.

If this leads to an “unbundling” as it did in retail, where consumers start going to different systems for different forms of care, this will lead to increased fragmentation in the short term. Partnerships and coordination of care across an ecosystem will become increasingly important for providers’ success.

4. Expect a new focus on experiences and non-price differentiators

In response to the rise in price transparency, both travel and retail responded by investing in winning on non-price features and obscuring the role of price in consumer shopping. Travel companies in particular increasingly started competing on experience and other value drivers, with loyalty programs becoming critical drivers of enterprise value. Marketing and advertising for travel companies focus on the overall travel experience and focus on differentiators like cabin quality (United’s Polaris) or reasons for travel (Southwest’s “Get away” campaign).

Similarly, retailers introduced exclusivities to make like-to-like comparisons harder - things like special editions, or replacing national brands with the company’s brand products. Further, retailers also invested in their store experience, with things like samples or better packaging to further complicate a consumer’s judgment of what the price was really purchasing.

How This Would Look in Healthcare

The parallels for Healthcare are quality, total value (inclusive of downstream costs), and consumer experience. Where providers seek to differentiate on quality or total value, they will increasingly need to prove it with data - not easily done today. They will need to prove it on dimensions that matter to consumers, which are not always the dimensions that matter to clinicians. The role of experience will surely rise. Those who can balance an affordable price position with making it incredibly easy for consumers to get their needs met and/or offering unique, hallmark experiences will win and keep consumers coming back.

5. Providers will shape how transparency evolves by proactively leading the charge

Just as the airlines once faced disruption from the online booking engines, so to do provider networks face potential disruption from new entrants looking to drive value from the regulations around price transparency. However, healthcare may want to similarly follow Aviation’s lead and NOT defer to new entrants to fill the gap for a consumer shopping utility. Few may remember it now, but Orbitz.com was not an independent disruptor. United Airlines, Delta Air Lines, Continental Airlines, Northwest Airlines, and later, American Airlines invested to start the company and provide a counter to the independents like Travelocity and Expedia. The benefit of entering directly was that the airlines were able to create something more valuable to the consumer, while also controlling the governance, bylaws, and rules of engagement in ways that were more advantageous to them.

How This Would Look in Healthcare

Now is the time for providers to decide how much they will support the shift to transparency. Even more than aviation, where the product is more directly comparable, it is easy to see how healthcare providers could come together to create a far more valuable platform than an uninformed third party. Doing so will accelerate competitive pressures but create long-term benefits by shaping how price/value transparency plays out.

6. New business models will arise to solve consumer pain points

In both retail and travel, technology and new business models both drove the increased price transparency, and then leveraged them to create ever more business models to capitalize on that transparency.

In retail, aggregators (like price comparison sites) were first. Then came integrators (like Instacart, that help execute your shopping for you). Then came innovators (like Jet.com that—for a time—aimed to create a whole new way to price by shopping across e-commerce sites). The commonality here is that one company streamlines all the different prices to snag the consumer the best deal possible, without the consumer having to do the heavy lifting in terms of research. Said otherwise, new businesses are looking to unbundle your purchasing without the hassle.

As we speak, the retail industry is under a huge upheaval from all these changes. Price transparency is playing an important role in shaping future strategies for retailers: a historically powerful lever for growth and profit, pricing, is increasingly taking a backseat. Now, you’re seeing emerging players focus on the shopping experience (like building shopping lists off your favorite recipes and your lifestyle choices).

How This Would Look in Healthcare

For healthcare, the many future business models that may be introduced are still too early-stage to fully anticipate. However, service companies already exist that help consumers navigate complex care episodes, make sense of medical bills, and advocate or negotiate on their behalf. Price transparency will help these intermediaries achieve higher scale and evolve to offerings like end-to-end shopping, broader financial advocacy, and customized experiential bundling for all care and non-care components. Domestic and international medical tourism will rise as these players approach consumers in high-cost markets with offerings for low cost, high-value care in cheaper markets, wrapped with luxury experiences. Together, this unbundling of care that is seamless to a patient could mirror what is happening in retail.

7. Not all lessons are repeatable

With the rise in transparency, retail’s era of promotions kicked into a higher gear. Personalized product and service options became the rage. In the meantime, e-commerce created a way to take what was a mass offer (the price you see in the store is what everyone, everywhere pays), to a personalized offer (if you buy this item online compared to in our actual store, it will be cheaper). Technology then became a gateway or sorts to individualized programs. In aviation, loyalty programs became essential to drive stickiness with consumers.

How This Would Look in Healthcare

We’re unlikely to see the same kind of deal-based trading in healthcare the way we see it in retail or the same loyalty incentives you see in aviation. The combination of contracting regulations and the potential risk of being perceived as pushing unnecessary care or favoring higher-income consumers will make these less applicable for the healthcare industry.

Looking Ahead

Stay tuned. In future articles we’ll publish here on Oliver Wyman Health, we’ll move beyond price transparency to value transparency, and we’ll consider how providers and payers can respond to evolving industry change and maximize impact.