Healthcare 2030: Four Economic Scenarios

Editor's Note: Since publication of this article in early 2019, the novel coronavirus pandemic has impacted the world. The ideas below clearly have new layers of relevance when applied to healthcare's current economic landscape as COVID-19 continues to evolve. The economic scenarios the industry will face in 2020 and beyond will continue to be a key discussion topic for leaders, especially as things like market shifts and the upcoming US election unfold.

There are a few claims we’re making (with confidence!) about healthcare’s future. We predict healthcare’s migration to value will continue. Margin pressure and intense competitive pressure will push efficiency among incumbents (like automating and transitioning care to lower acuity environments). Industry boundaries will be challenged as digital, retail, and other companies make deeper forays into healthcare. But how fast will change happen? And who will win (and lose) profit share?

Looking back on how the industry has progressed over the last two decades, US healthcare now comprises 18 percent of total gross domestic product, up 13 percent from twenty years ago. The composition of that spending has remained (remarkably) stable since 1960, with 38 percent to hospitals, 23 percent to physician services, and 12 percent to prescription drugs. Pharma accounts for less than one-sixth of total healthcare spend, while deriving almost half of healthcare ecosystem profits.

Is this share of profits in the industry stable, or is it about to be turned upside down over the next decade? Below, we examine the range of possible scenarios.

Key Questions Driving Our 2030 Scenarios

1. Will the move to value continue at the same pace?

2. Will healthcare costs increase faster than the system can bear?

3. Will the government aggressively demand change?

4. Where will most tech-driven innovations originate and who will monetize them?

5. Will incumbents or out-of-industry players invest more in (building and/or acquiring) innovation?

6. How empowered and motivated will consumers be to “vote with their wallets” for better healthcare?

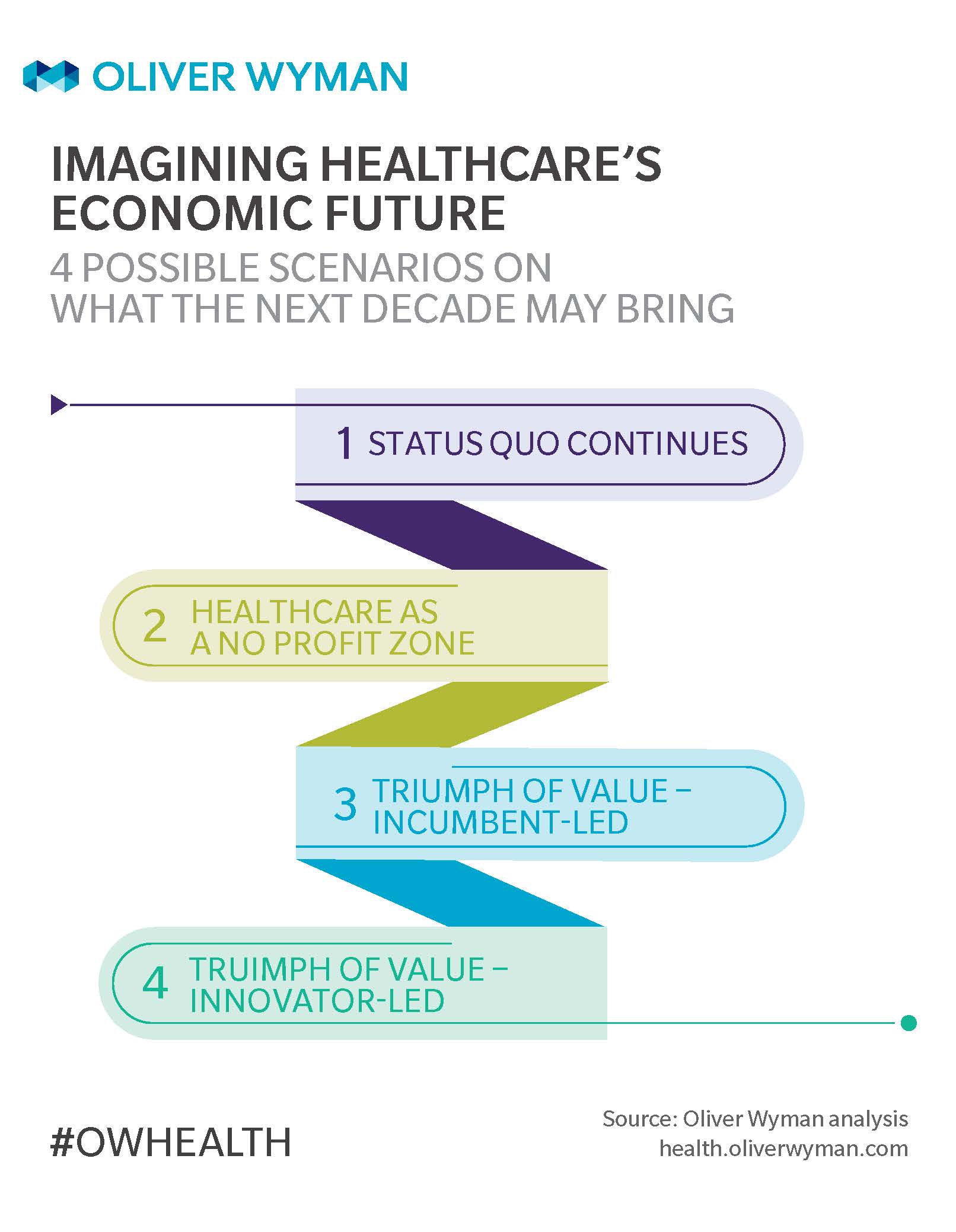

Four Future Scenarios

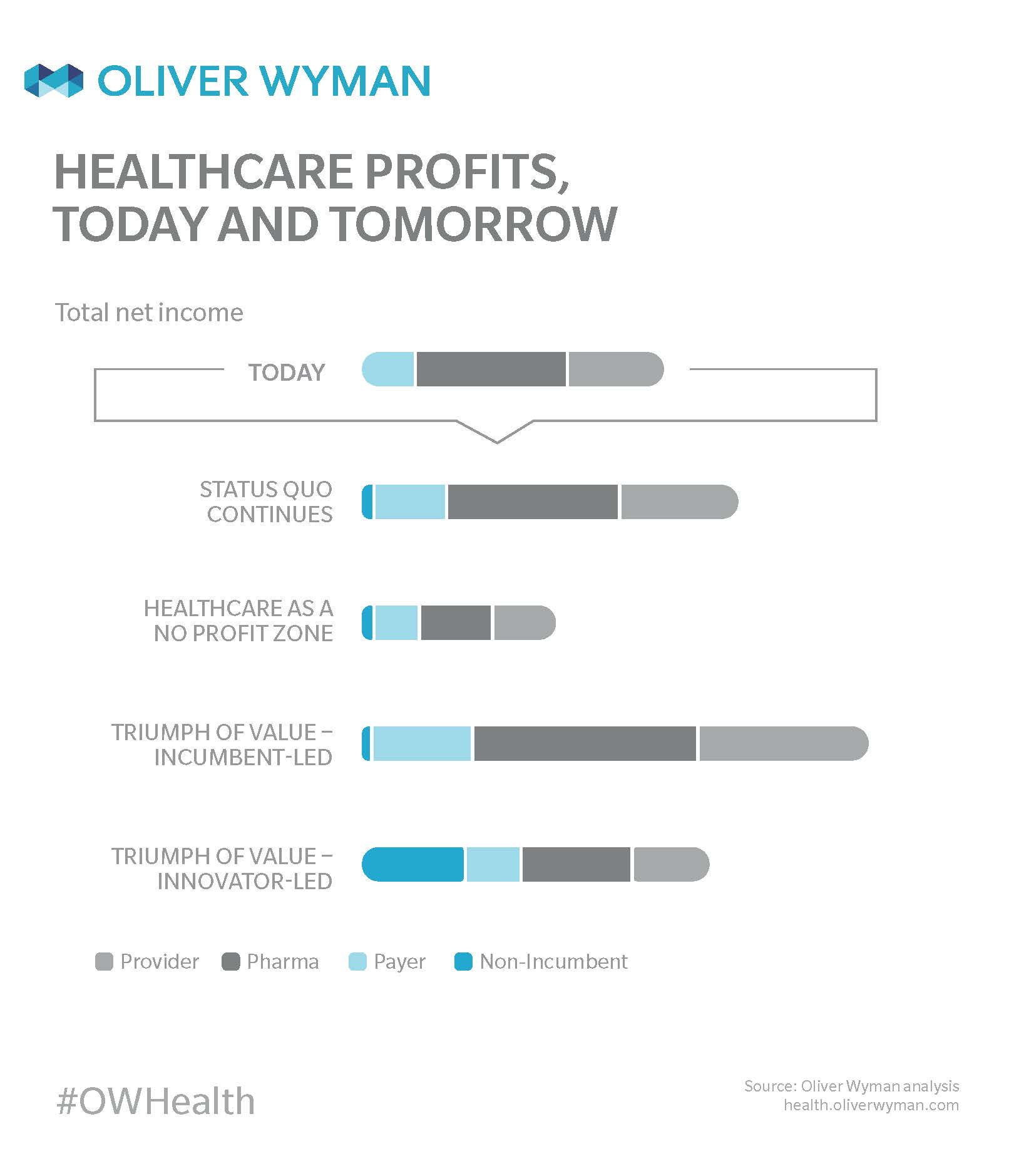

Scenario 1: Status Quo Continues

Here, the next decade closely mirrors the last. Total healthcare costs increase before levelling off with gross domestic product growth. Value-based reimbursement models become only slightly more common. Healthcare’s still primarily fee-for-service. Government deficits continue, but Medicare and Social Security remain solvent.

Incumbents still create incremental efficiency through consolidation and process improvement. Most improvements are uniform, maintaining competitive parity without providing undue advantage to new business models. Electronic Health Record penetration reaches maturity, creating process efficiencies and modest clinical management improvements, reducing unnecessary medical costs.

Payers’ progress is evolutionary. They create simpler, more flexible products featuring integrated ancillary coverage, sculpted networks, and other cost-cutting levers. Care management programs slowly improve. Payer business models aren’t fundamentally disrupted.

Providers see continued inpatient to outpatient migration, from higher to lower acuity, from general to more highly specialized Industrialized Factory environments, driving better consumer experiences and lower costs, without fundamentally disrupting business models. These improvements cancel out net increases in healthcare demand. Provider compensation grows, although slower than before.

On the life sciences side, a modest number of new blockbuster treatments emerge (as neurology joins oncology and immunology as a critical source of profit growth), roughly offsetting patent expirations. Pharma sparks meaningful innovation, enabling medical advancements that drive economic value. In areas with profit headwinds like diabetes and cardiology, pharma companies integrate new non-product-based offers, like behavior change programs.

Next-generation delivery models (like Iora, Amazon, and Omada) with potential for massive disruption exist, but still at the margins. Innovation happens in pockets. Nobody develops scalable, innovative solutions. Costs increase, but not faster than the system can withstand. Medicare and Social Security remain solvent. Industry economics are largely unchanged.

This scenario may seem unlikely. But if we’d written these words in 2009, it’s this scenario that would have best described the next ten years, where innovations and improvements happen in silos without fundamentally changing healthcare’s economic landscape.

Scenario 2: Healthcare As A No Profit Zone

This scenario begins like the last, but with less optimistic macroeconomics. The industry cannot drive incremental value without fundamentally disrupting existing business models. Government deficits skyrocket. Continued increase in deductibles and out-of-pocket spend oppresses patients, driving political reform. As a result, there’s a “reckoning” five years out, when rising healthcare costs become unbearable.

Medicare and Medicaid reimbursement is reduced, hitting pharma hard, as the government targets drug reimbursement parity with Organisation for Economic Co-operation and Development (OECD) countries. Annual prescription drug price increases disappear. More stringent limitations regarding comparative effectiveness limit new drugs coming to market. The government launches a “Medicare for all” single payer option which is managed similarly to Medicare Fee-for-Service, where payers play only a small, back office processing role. And thus, payers lose most of their commercially insured members to Medicare, now a direct competitor. Employers, eager to reduce costs and offer lower premiums and deductibles, contract directly with providers for the remaining commercial business, further dwindling legacy payer membership.

Incumbents’ margins are dramatically compressed. Consolidation pushes as far as regulators allow, leaving a few incumbents with razor thin margins, as price and earnings multiples enter mid-single digits. Like Scenario 1, innovative start-up and out-of-industry solutions exist in pockets, but aren’t profitable, or scalable enough to disrupt. Despite enough well-funded investors to spark competition and drive lower prices, a killer solution doesn’t thrive and prosper in the end.

Scenario 3: Triumph of Value – Incumbent-Led

Several “vectors to value” reach critical inflection points, going from pilots and silos to disruptors. Market incumbents lead the way. This creates massive consumer value and significantly expands healthcare profit pools, increasing opportunities to harness value for both incumbents and new market entrants. “Value” broadly includes supply-side and demand-side innovations driving better outcomes and lower cost of care, including vectors like:

- Behavior: Behavior change companies go to market with new psychologically nuanced, magnetic behavior change programs so compelling, many consumers willingly pay for them (instead of being paid to participate). These Automated Agents leverage a data explosion to personally remind and nudge consumers toward healthy behaviors. A mainstream “healthy living culture” emerges. Chronic disease rates drop. Consumer peer pressure to stay healthy spikes.

- Tech: A new killer app takes charge, like how Apple transformed technology. A centralized platform guaranteeing excellent consumer experience manages all consumer interactions with the healthcare system.

- Tools: The healthcare ecosystem achieves nearly optimal incentives across stakeholders and universal access, creating necessary tools that drive best practitioner choices. Industrialized Factories compete to deliver the highest quality, lowest cost care possible, leading to more efficient best practices and standardization. Integrated Patient Managers are strongly incentivized to manage highly complex patients and more innovatively and efficiently deliver care.

- Science: Headline-grabbing technologies (like genomics, personalized medicine, and robot caregivers) become mainstream faster than predicted. Genomics, particularly, drives a step change in healthcare outcomes as new breakthrough therapies come to market, commanding large pharma premiums. Scientific advances make personalized prevention the norm in many disease areas.

- Delivery: Virtual and bricks and mortar healthcare experiences become almost fully interchangeable for all but the highest acuity care episodes. Access Specialists systematically deliver convenient care though new delivery channels.

The “Behavior” and “Tools” vectors mentioned above (where healthcare incumbents already play) may prove triumphant, but incumbents also leave their comfort zones for other vectors. Incumbents maintain financial footing long enough to fuel healthy innovation investments and leverage core strengths like healthcare financing control, healthcare data access, and point of care proximity.

The “brave new world” of genetic and personalized medicine creates a new sub-industry for life sciences and device companies. Payers leave underwriting and risk taking for healthcare data science, behavior change, and managing an “iPhone-like” integrated healthcare experience. Highly performing providers heavily incentivized for cost and quality achieve massive gainsharing. Across these industries, incumbents hyper-aggressively acquire new innovations that drive transformation.

Just like how biotech drove significant clinical value two or three decades ago, pharma – with 40 percent of value capture thanks to new developments in artificial intelligence, genomics, gene science, personalized therapy, and the like – captures value and withstands price pressure.

Scenario 4: Triumph of Value – Innovator-Led

Like Scenario 3, several “vectors to value” reach critical inflection points, but this time driven by new market entrants.

Healthcare majorly pivots towards consumerism; the “Behavior”, “Tech”, and “Science” vectors initially dominate. Brand power, engagement, and strong consumer relationships become primary differentiators. Magnetic platform owners creating quality consumer experiences accrue value. Amazon and/or smart phone apps provide integrated consumer solutions to find doctors, purchase insurance, and change behaviors, leading to healthier lives. New market entrants capitalize on customer relationships to provide more traditional healthcare services, playing in the “Tools” and “Delivery” vectors. Increasingly, these solutions lead patients to healthcare’s “new front door” through retail clinics or virtual care owned and operated by new entrants. Incumbent business models remain largely stagnant, relegated to suppliers highly detached from customers.

Health insurers and traditional providers are commoditized, “racing to the bottom” to offer the lowest prices for services where patients use digital comparative shopping tools. Patients are loyal to the platform, not payers and providers (now secondary vendors). In an extreme case, the traditional healthcare system becomes a last resort destination as patients seek virtual care or retail clinic options, for all but the highest acuity care episodes. Low acuity care is no longer considered “healthcare”, but a consumer service provided by a mix of retail and Internet companies.

For incumbents, results mirror the “Health as a No Profit Zone,” Scenario 2 as they cede wallet share to out-of-industry players, now earning only a small profit portion in healthcare’s new market. Meanwhile, companies considered “non-healthcare” in 2019 will accumulate well over a trillion dollars in healthcare market cap by 2030.

In the future, different scenarios will increase value with highly contrasting implications for profit shares. Those who understand trends, vectors, and how to create strategic control and value will be best positioned. 2030, here we come.